Mortgage Rate Outlook

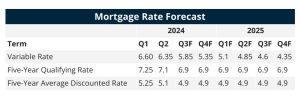

BRITISH COLUMBIA – Now that the Bank of Canada is lowering its policy rate, there is some expectation that fixed mortgage rates should also fall. However, the impact on fixed mortgage rates going forward may not be that significant.

The reason is that the bond market, and by association, the mortgage market, is like a machine that digests all available information about current and future economic conditions. Since late 2023, markets have strongly anticipated falling policy rates. As a result, five-year fixed mortgage rates have likely already priced in the entirety of expected rate cuts.

Another way to think about this is that the spread between the overnight rate and five-year fixed mortgage rates needs to normalize. Historically, that spread has averaged around 225 basis points. At a rate of 2.75 per cent, the expected final destination for the Bank’s policy rate, that would equate to a five-year fixed rate of about 5 per cent.

That means that even as the Bank of Canada starts to lower its policy rate, there may be very little downward movement in five-year fixed mortgage rates from where they are now. Moreover, the five-year bond yield is often more influenced by US economic data and expectations for US monetary policy than by the Bank of Canada. As such, borrowing costs could still rise modestly even as the Bank cuts rates if economic conditions or inflation in the United States improve unexpectedly.

As for variable rates, current market pricing has settled around prime minus 60 basis points. If that discount holds, it will take seven rate cuts, or a 175 basis point decline before the average variable rate falls under the average five-year fixed rate.

Economic Outlook

Real GDP rose 1.7 per cent in the first quarter on an annualized basis, following a negatively revised no growth in the fourth quarter of 2023. That revision means that Canada very narrowly avoided a technical recession in 2023.

Negative revisions to past GDP growth and below-forecast first-quarter growth are yet another piece of evidence supporting the Bank’s decision to cut rates. Soft real GDP growth in Canada looks worse when one considers the very rapid rate of population growth; real GDP per capita continues to decline sharply.

This comes in the context of excellent progress on inflation, which hit 2.7 per cent last month, and looks even better when one digs deeper into the CPI report. Price appreciation now boils down almost entirely to rent and mortgage costs. The labor market in Canada also continues to soften, with the unemployment rate hitting 6.2 per cent last month while job vacancies continue to fall.

We expect that growth in the Canadian economy will remain weak for much of 2024, leading to a further uptick in the unemployment rate before a gradual loosening of monetary conditions spurs growth in 2025.

Bank of Canada Outlook

This Bank of Canada rate-lowering cycle is one of the few times this century that the Bank has not lowered rates in response to a global crisis. As such, we should expect a gradual pace of rate cuts measuring 25 basis points per meeting over the next 18 months until the Bank’s policy rate hits the midpoint of the Bank’s estimated neutral range of 2.25-3.25 per cent. Where the policy rate ultimately ends up will be dictated by economic conditions. A good baseline is 2.75 per cent, but a worse-than-expected economy could mean the Bank’s policy rate needs to fall under 2.25 per cent for a period. Conversely, more stubborn-than-anticipated inflation could mean this lowering cycle stalls north of 3.25 per cent.

While there is uncertainty about where the Bank’s policy rate may be by the end of next year, there is virtually no case for leaving rates unchanged. Inflation has had significant downward momentum and the labor market is weakening. We estimate that if the Bank were to delay rate cuts by one year, inflation would substantially undershoot the Bank’s 2 per cent target at the cost of job losses and much higher unemployment. Clearly, the Bank of Canada sees similar risks of keeping policy too tight, hence the commencement of rate cuts in June.