James Mabey, CREA Chair

OTTAWA – While there were early signs of renewed momentum in June following the Bank of Canada’s first interest rate cut since 2020, activity in Canada’s housing market took a pause in July.

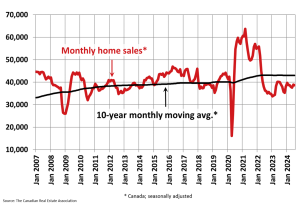

Home sales activity recorded over Canadian MLS® Systems edged back by 0.7% on a month-over-month basis in July 2024, giving back a small portion of June’s post-first rate cut gain. (Chart A)

“With another rate cut announced on July 24, we’ve now seen two rate cuts in a row, and the expected pace of future policy easing has steepened considerably, with markets now anticipating rate cuts at every remaining Bank of Canada decision this year,” said Shaun Cathcart, CREA’s Senior Economist. “Combine that with a record amount of demand waiting in the wings, and the forecast for a rekindling of Canadian housing activity going into 2025 has just gone from a layup to a slam dunk.”

Monthly changes in sales activity were generally small amongst the larger centres in July. Interestingly, declines in Calgary and the Greater Toronto Area were mostly offset by gains in Edmonton and Hamilton-Burlington.

As of the end of July 2024, there were about 183,450 properties listed for sale on all Canadian MLS® Systems, up 22.7% from a year earlier but still about 10% below historical averages of more than 200,000 for this time of the year.

New listings posted a slight 0.9% month-over-month increase in July. The national increase was led by a much-needed boost in new supply in Calgary.

With new listings up slightly and sales down slightly, in July, the national sales-to-new listings ratio eased back to 52.7% compared to 53.5% in June. The long-term average for the national sales-to-new listings ratio is 55%, with a sales-to- new listings ratio between 45% and 65% generally consistent with balanced housing market conditions.

“While it wasn’t apparent in the July housing data from across Canada, the stage is increasingly being set for the return of a more active housing market,” said James Mabey, Chair of CREA. “At this point, many markets have a healthier amount of choice for buyers than has been the case in recent years, but the days of the slower and more relaxed house hunting experience may be somewhat numbered.”

There were 4.2 months of inventory on a national basis at the end of July 2024, unchanged from the end of June. The long-term average is about five months of inventory.

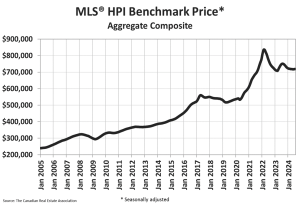

The National Composite MLS® Home Price Index (HPI) edged up 0.2% from June to July. While a small increase, it was slightly larger than the June increase, making it just the second, and the largest, gain in the last year. (Chart B)

While prices were up slightly at the national level, they were held back by reduced activity in the largest and most expensive British Columbia and Ontario markets. Regionally, prices are rising in a growing number of markets – a majority at this point.

The non-seasonally adjusted National Composite MLS® HPI stood 3.9% below July 2023. This mostly reflects how prices took off last April, May, June, and July – something that was not repeated over that same period in 2024. It’s mostly likely that year-over-year comparisons will improve from this point on.

The actual (not seasonally adjusted) national average home price was $667,317 in July 2024, almost unchanged (-0.2%) from July 2023.

The Canadian Real Estate Association (CREA) is one of Canada’s largest single-industry associations, representing more than 160,000 Realtors® working through 69 real estate boards and associations.