Chart A

OTTAWA – Activity in Canada’s housing market saw some early signs of renewed life in June 2024, following the Bank of Canada’s interest rate cut at the beginning of the month.

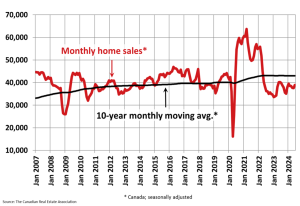

Home sales activity recorded over Canadian MLS® Systems climbed 3.7% between May and June 2024. (Chart A)

“It wasn’t a ‘blow the doors off’ month by any means, but Canada’s housing numbers did perk up a bit on a month-over-month basis in June following the first Bank of Canada rate cut,” said Shaun Cathcart, CREA’s Senior Economist. “Year-over-year comparisons don’t look great mainly because of how many buyers were still jumping into the market last spring, but that’s a story about last year. What’s happening right now is that sales were up from May to June, market conditions tightened for the first time this year, and prices nationally ticked higher for the first time in 11 months.”

As of the end of June 2024, there were about 180,000 properties listed for sale on all Canadian MLS® Systems, up 26% from a year earlier but still below historical averages of around 200,000 for this time of the year. On a seasonally adjusted basis, the end-of-June supply number was only up 0.5% from the end of May, suggesting the national inventory buildup may be slowing down.

New listings posted a 1.5% month-over-month increase in June, led by the Greater Toronto Area and British Columbia’s Lower Mainland.

As the national increase in new listings was smaller than the sales gain in June, the national sales-to-new listings ratio tightened to 53.9% compared to 52.8% in May. The long-term average for the national sales-to-new listings ratio is 55%, with a sales-to-new listings ratio between 45% and 65% generally consistent with balanced housing market conditions.

“The second half of 2024 is widely expected to see the beginnings of a slow and gradual return of buyers into the housing market,” said James Mabey, Chair of CREA. “Those buyers will face a considerably different shopping experience depending on where they are in Canada, from multiple offers in places like Calgary, to the most inventory to choose from in over a decade in places like Toronto.”

There were 4.2 months of inventory on a national basis at the end of June 2024, down from 4.3 months at the end of May. It was the first time that the number of months of inventory has fallen month-over-month in 2024. The long-term average is about five months of inventory.

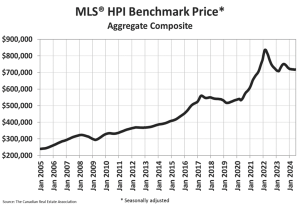

The National Composite MLS® Home Price Index (HPI) inched up 0.1% from May to June. While a small increase, it was noteworthy in that it was the first month-over-month gain in 11 months. (Chart B)

Chart B

Regionally, prices are still generally sliding sideways across much of the country. The exceptions remain Calgary, Edmonton, and Saskatoon, and to a lesser extent Montreal and Quebec City, where prices have steadily moved higher since the beginning of last year.

That said, there have been some more recent upward movements in prices in other markets, including across Ontario cottage country, Mississauga, Hamilton-Burlington, Kitchener-Waterloo, Cambridge, London-St. Thomas, and Halifax- Dartmouth.

The non-seasonally adjusted National Composite MLS® HPI stood 3.4% below June 2023. This mostly reflects how prices took off last April, May, June, and July – something that has not been repeated in 2024.

The actual (not seasonally adjusted) national average home price was $696,179 in June 2024, down 1.6% from June 2023.

Source: CREA